Introduction

This is a comprehensive financial calculator designed for UK tax residents, tailored for the 2026/27 tax year. It supports both employed (PAYE) and self-employed individuals to accurately calculate net income, student loan repayments, pension optimisation, and tax planning.

Key Features:

- Calculate net take-home pay

- Analyse multiple student loan plans (Plan 1/2/4/5 & Postgraduate)

- Optimise pension contributions (Salary Sacrifice vs. Relief at Source)

- Self-employed tax estimation & payment scheduling

- Debt vs. wealth trajectory forecasting

Quick Start

2.1 Select Your Employment Mode

Upon loading the page, first select your employment status. This determines which input fields are displayed.

- PAYE For individuals employed by a company

- Self-Employed For freelancers, contractors, or sole traders

2.2 Confirm Tax Year

Ensure the tax year displayed in the top-left corner reads 2026/27. This calculator is updated based on official HMRC and SLC rules.

Input Financial Details (PAYE Mode)

3.1 Income Details

Enter your gross annual salary

May push you into higher tax bracket

Used for cashflow projection

3.2 Student Loan Portfolio

3.3 Pension & Optimisation

💡 Pension Impact: Salary Sacrifice reduces Student Loan & NI calculations. Net Pay and Relief at Source do not.

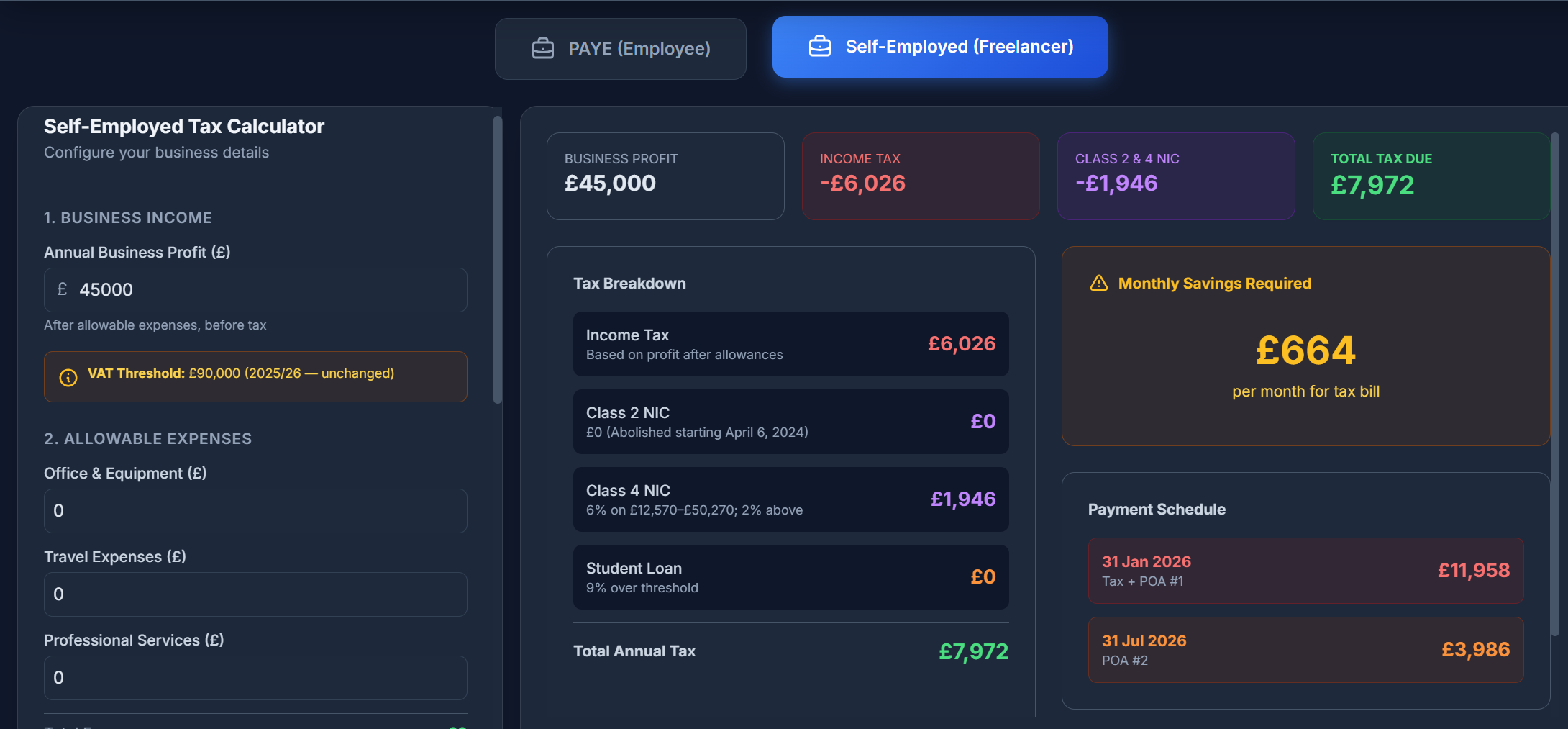

Input Financial Details (Self-Employed Mode)

4.1 Business Income & Expenses

After allowable expenses, before tax

£90,000 (2026/27 — unchanged)

4.2 Key Deadlines

Online Return

31 Jan 2026

Payment Due

31 Jan 2026

POA #2

31 Jul 2026

View Calculation Results Dashboard

Click Recalculate Dashboard

Generate your detailed financial report

Gross Pay (Mo)

£0

Income Tax

-£0

National Insurance

-£0

Student Loans

-£0

Take Home

£0

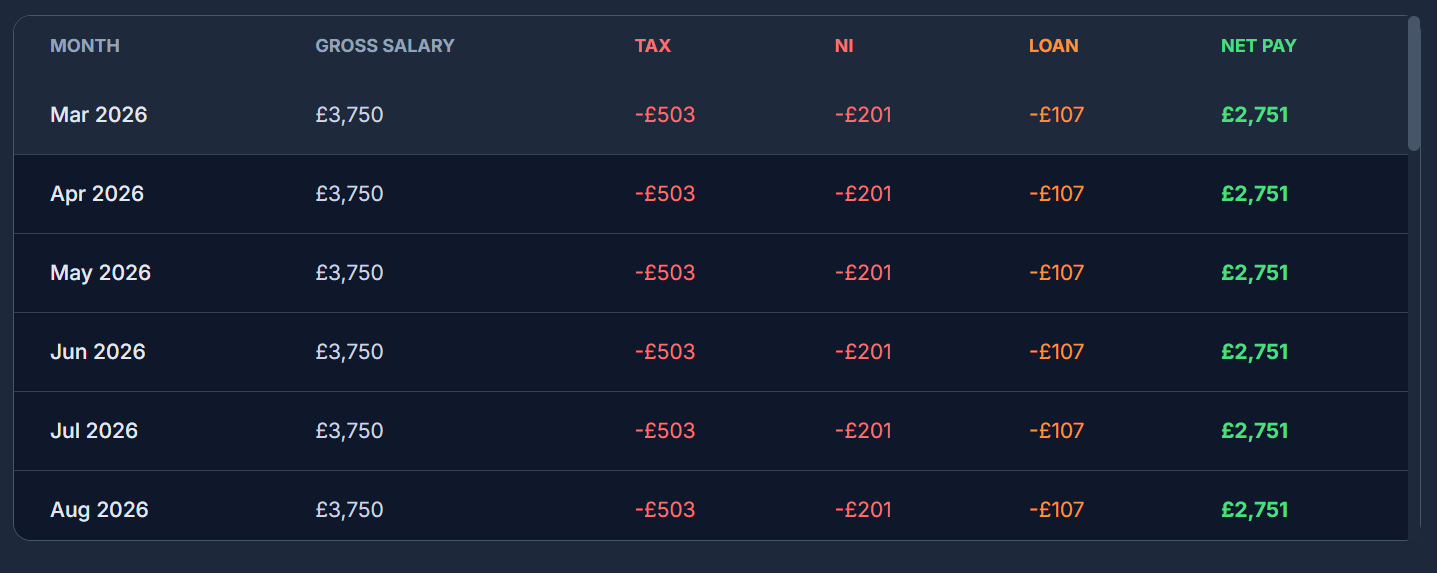

| Month | Gross Salary | Tax | NI | Loan | Net Pay |

|---|---|---|---|---|---|

| April | £0 | -£0 | -£0 | -£0 | £0 |

| May | £0 | -£0 | -£0 | -£0 | £0 |

| June | £0 | -£0 | -£0 | -£0 | £0 |

Advanced Strategies & Optimisation

Lie Flat

Wait for 30/40 year write-off.

Total Interest

£0

Aggressive

Pay extra £200/mo to clear debt.

Interest Saved

£0

ISA Investor

Invest extra £200/mo at 5% return.

ISA Value (10y)

£0

💡 Smart Insight

Pension Boost Scenario: Increasing pension by 2% reduces loan repayment by £25/mo while adding £80 to your pot.

Reference Guide & FAQ

The Personal Allowance is £12,570 — the amount you earn before paying income tax. It tapers by £1 for every £2 earned above £100,000, disappearing at £125,140. This creates an effective 60% marginal rate in that band. Pension salary sacrifice can pull your income back below £100k to restore it.

Salary Sacrifice reduces gross pay before tax and NI are calculated — saving on both. Relief at Source uses net pay; HMRC then adds 20% basic-rate relief automatically, but higher-rate taxpayers must claim the extra 20–25% via self-assessment. Salary Sacrifice also reduces student loan repayments since those are income-based.

For every £2 earned between £100k–£125,140, you lose £1 of Personal Allowance. Combined with 40% income tax, the effective marginal rate is 60%. The most efficient solution is pension salary sacrifice — it reduces gross income, potentially pulling you below £100k and restoring your full allowance. Gift Aid donations have a similar effect.

Yes. Student loan repayments are 9% of income above your threshold. Salary sacrifice lowers your gross income, so the repayable amount shrinks too. Example: earn £35,000, sacrifice £5,000 into pension → repayable income drops to £30,000. On Plan 2 that saves you 9% × £5,000 = £450/year in loan repayments, on top of income tax and NI savings.

Important Notes & Disclaimer

- Accuracy: This tool is based on official HMRC and SLC rules but is for guidance only—not financial or tax advice.

- 60% Tax Trap: Income between £100k–£125,140 incurs an effective marginal rate of ~60% due to Personal Allowance taper. Use pension Salary Sacrifice to mitigate.

- Self-Employed Payments: Remember Payments on Account (POA); consider setting aside 25–30% of monthly profit for tax.

- Updates: This guide reflects 2026/27 rules; thresholds may change with future government budgets.

Sources: HMRC, SLC, GOV.UK — 2026/27. For guidance only; not financial or tax advice.

Appendix: 2026/27 Key Data Quick Reference

Tax Thresholds

| Band | Rate | Income up to |

|---|---|---|

| Personal Allowance | 0% | £12,570 |

| Basic Rate | 20% | £50,270 |

| Higher Rate | 40% | £125,140 |

| Additional Rate | 45% | No limit |

Key Allowances

| Item | Value |

|---|---|

| Personal Allowance | £12,570 |

| ISA Annual Allowance | £20,000 |

| Pension Annual Allowance | £60,000 |

| VAT Registration Threshold | £90,000 |

Student Loan Plans

| Plan | Who | Threshold | Rate | Write-off |

|---|---|---|---|---|

| Plan 1 | Pre-2012 Eng/Wales/NI | £26,065 | 9% | 25 yrs / age 65 |

| Plan 2 | 2012–Aug 2023 Eng/Wales | £28,470 | 9% | 30 years |

| Plan 4 | Scotland (post-1998) | £32,745 | 9% | 30 yrs / age 65 |

| Plan 5 | Post-Aug 2023 Eng/Wales | £25,000 | 9% | 40 years |

| Postgrad | Master's / Doctoral | £21,000 | 6% | 30 years |

Note: All data above is built into the calculator—no manual calculation required. Use this table for quick reference only.